This article, Financial Foundation pillar, is the first of four pillar guides within the FREE Financial Freedom Framework. If you have not read the overview yet, start there – it explains how the four pillars work together.

Financial Foundation Pillar - What It Is and Why It Comes First

When people think about improving their finances, they almost always never start with Financial Foundation. They look at investments, side incomes, or savings targets. However, the question that matters most is much simpler.

Can you manage day-to-day life without constant financial stress?

That is what a financial foundation is. It is not about how much you earn. It is not about having a budget that accounts for every penny. It is the quiet confidence that comes from knowing where your money goes, having enough of a buffer to absorb the routine surprises that every month brings, and being clear about what you actually need versus what you have been told you should want.

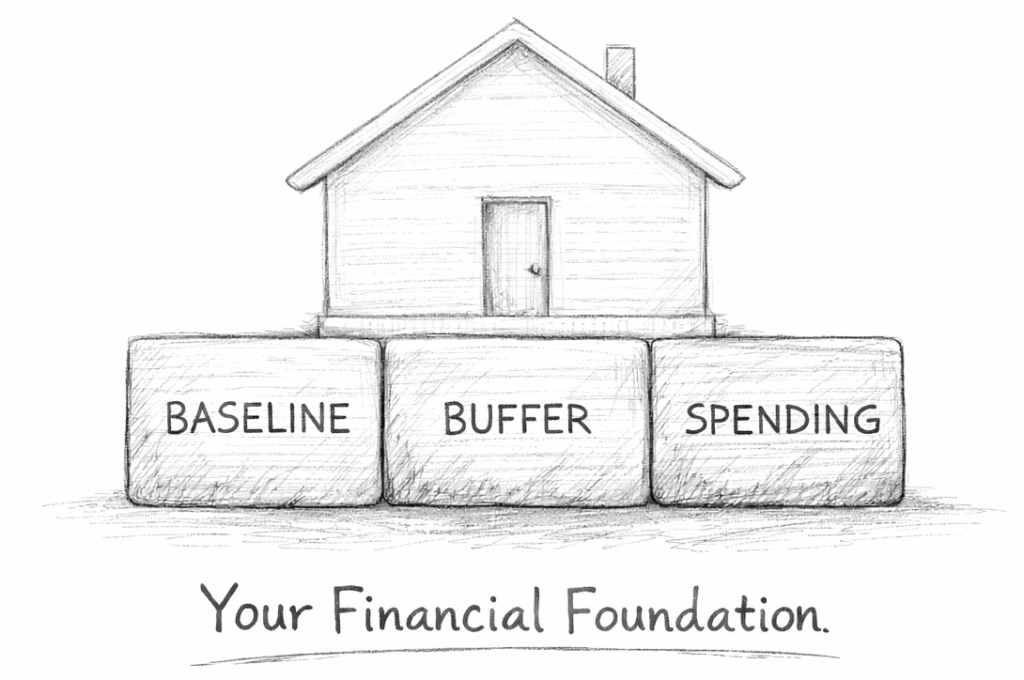

Think of it like a building.

Everyone wants to discuss the layout, the views, and the finishing touches. Very few people get excited about the foundations underneath. But without them, nothing above ground is safe. Every improvement, every addition, every plan sits on top of that base. If it is weak, everything else feels fragile – no matter how impressive it looks from the outside.

Most financial frameworks skip this step entirely. They assume the base is already in place and move straight to growth, investment, or debt reduction strategies. For many people, that is precisely why those strategies fail.

A strong financial foundation changes the way every other money decision feels.

Why Most People Skip Foundation

There is a reason so many people jump past this step. Foundation work does not feel exciting. It does not produce dramatic results. Nobody posts about finally understanding their baseline monthly costs, and there is no visible milestone when a genuine one-month buffer is in place.

More than that, looking closely at your finances can feel genuinely uncomfortable. If you have been avoiding the numbers – and many people have – the act of sitting down and seeing where things actually stand can feel like a confrontation.

It is tempting to skip straight to the part that feels like progress: investing, earning more, or chasing a financial goal that sounds impressive.

This avoidance is not a character flaw. Research consistently shows that financial uncertainty activates the same stress pathways as physical threats. When your brain senses a potential problem it cannot quantify, it defaults to avoidance. Not looking becomes a way of managing anxiety, even though it makes the underlying situation worse over time.

The irony is that the act of looking – of simply understanding where you stand – is often the thing that reduces the anxiety most.

Clarity is not the reward that follows hard work. It is the starting point that makes everything else manageable.

What a Financial Foundation Looks Like in Practice

Foundation is not a single action. It is a set of conditions that, when present, remove the low-level financial stress that so many people carry without even realising it.

Know Your Baseline

Understand your real monthly costs

Build a Buffer

One month of baseline in accessible savings

Align Your Spending

Ensure spending reflects your actual priorities

See Where Your Foundation Stands

The Financial Freedom Score takes less than five minutes and shows you exactly where you are across all four pillars – starting with Foundation.

Knowing Your Baseline

Your baseline is the amount you need each month to live your current life – not the life you aspire to, not the life you had five years ago, but the one you are actually living right now. This includes housing, utilities, food, transport, insurance, and any recurring commitments.

Most people do not know this number with any accuracy. They have a rough sense, but the gap between what they think they spend and what they actually spend is often significant. That gap is a source of background stress, because decisions are being made without a reliable foundation of information.

Knowing your baseline is not budgeting in the traditional sense. It is not about restricting yourself or tracking every transaction. It is simply about having an honest picture.

Once that picture exists, decisions that previously felt heavy begin to feel clearer.

Having a Genuine Buffer

A buffer is money set aside for the routine surprises that every month brings. Not emergencies – those fall under Resilience. A buffer handles the predictable unpredictability of normal life: the car service that comes earlier than expected, the appliance that needs replacing, the school trip payment you forgot about.

Without a buffer, every unexpected cost becomes a small crisis. The stress is not about the amount – it is about the disruption. When there is no margin, even modest surprises force difficult choices, and those choices accumulate into a feeling of being perpetually behind.

A buffer does not need to be large. Even one month of baseline costs set aside in an accessible account changes the experience of daily life. The numbers may not look dramatically different, but the feeling shifts considerably.

Clarity About Needs Versus Noise

Modern life produces an extraordinary amount of financial noise.

Subscription services, lifestyle inflation, comparison with peers, marketing that frames wants as necessities – all of these erode foundation without any single one of them feeling significant on its own.

Building a financial foundation includes a quiet audit of what genuinely serves your life and what has accumulated through habit or external pressure. This is not about deprivation. It is about alignment. When your spending reflects your actual priorities rather than inherited assumptions, the same income goes further – and the sense of control it brings is disproportionate to the money saved.

Foundation Is Not Budgeting

This distinction matters. Budgeting, as most people experience it, is about control – allocating categories, tracking spending against limits, and feeling guilty when numbers do not match. For many people, budgeting increases financial stress rather than reducing it, because it adds another system to maintain and another way to feel like you are falling short.

Foundation takes a different approach. Rather than controlling every line, it focuses on three things: knowing your baseline, having a buffer, and ensuring your spending reflects your real priorities. Once those conditions are met, the details tend to sort themselves out. You do not need to know that you spent exactly fourteen pounds on coffee last week. You need to know that your essential costs are covered, your buffer is intact, and nothing in your regular spending is quietly undermining your stability.

Think of it as the difference between micro-managing every employee in a team and making sure the right people are in the right roles. Both involve managing, but one creates constant tension while the other creates space for things to work well on their own.

What Foundation Looks Like at Different Stages

One of the key principles of the FREE Framework is that the pillars are not sequential steps to complete in order. They are dimensions of financial health that shift in importance as life changes. Foundation is always relevant, but what it means in practice changes considerably.

Early Career

For someone in their twenties or early thirties, foundation work often means building clarity for the first time. Understanding what you actually spend. Creating even a modest buffer. Learning the difference between spending that serves your life and spending that simply happens by default.

At this stage, the most valuable outcome is not a specific savings number – it is the habit of paying attention. Getting comfortable with your financial reality while the stakes are relatively low builds a pattern that serves you for decades.

Mid-Career

In your thirties and forties, foundation often needs recalibrating. Income has typically grown, but so have commitments: housing costs, dependents, insurance, lifestyle inflation that accumulated gradually. Many people at this stage earn significantly more than they did ten years ago yet feel no more stable, because their baseline has risen to match.

This is where foundation work can feel uncomfortable but is most valuable. Recalculating your true baseline – not the one from three years ago -often reveals that financial pressure is not coming from insufficient income but from costs that expanded without deliberate choice.

Pre-Retirement and Beyond

As income sources change approaching and entering retirement, foundation takes on a different character. The baseline itself shifts: some costs disappear (commuting, professional expenses) while others increase (healthcare, home maintenance).

What was stable for decades may need reassessing.

At this stage, foundation is about ensuring that the transition from earning to drawing down does not create a gap between what you need and what you have planned for. The clearer your baseline, the more confidently you can make decisions about pensions, drawdown strategies, and how to structure the next phase of life.

How Foundation Connects to the Other Pillars

Foundation does not exist in isolation. It is the base that the other three pillars rest on.

Without foundation, Resilience has no anchor. An emergency fund means little if you do not know your monthly baseline -how do you calculate how many months it covers?

Without foundation, Expansion feels like gambling. Investing while your day-to-day finances are uncertain is not growth. It is adding complexity to an already unstable situation.

Without foundation, Enjoyment carries guilt. Spending on things you value feels risky when you are not confident the essentials are covered. The permission to enjoy comes from knowing the base is solid.

This is why the FREE framework positions Foundation as the first pillar – not because everyone must start here, but because progress in any other pillar is more sustainable when the foundation is in place.

Where to Start

If reading this has made you realise that your financial foundation needs attention, that recognition is itself the first step. Most people carry vague financial unease for years without ever identifying exactly where it comes from. Simply naming the issue – “my baseline is unclear” or “I do not have a genuine buffer” – removes a surprising amount of the weight.

Here are three practical starting points.

Measure Where You Stand

The Financial Freedom Score is a free diagnostic tool that gives you a clear snapshot of your current financial health. It takes about 15 minutes, requires no email address, and runs entirely on your own device. Nobody else sees your numbers.

It will not tell you what to do – it will show you where you are.

Calculate Your Real Baseline

Look at three months of actual spending. Not what you think you spend – what you actually spend. The number may be higher than expected. That is normal, and it is useful information, not a reason for self-criticism.

Build A Small Buffer First

One month of baseline costs in an accessible account changes the texture of daily life. It does not need to be built overnight. Even setting aside a modest amount consistently moves you from fragility to stability faster than you might expect.

Ready to Measure Your Own Foundation?

Understanding the concept is step one. Knowing where you actually stand is step two. The Financial Freedom Score gives you a clear, honest picture in less than five minutes.

Continue Exploring the Framework

Foundation is the first pillar of the FREE Financial Freedom Framework, but it is not the only one. Explore the others when you are ready:

→ Resilience: Preparing for Change Without Living in Fear

→ Expansion: Growing Resources Without Reintroducing Stress

→ Enjoyment: Making Freedom Something You Actually Live

Or return to the FREE Framework overview to see how all four pillars work together.

Stability is not a destination. It is the ground you stand on while building everything else.